OVERVIEW

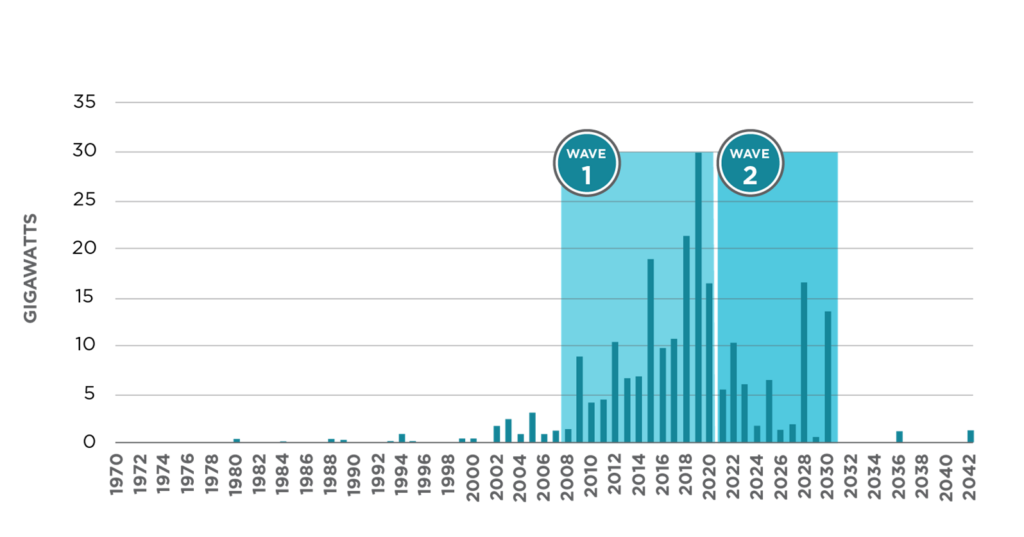

A second wave of coal plant closures is projected across the United States in the next five to ten years. The first wave began in the early 2000s and was driven solely by economic considerations. The second wave will be driven by similar economic considerations but buoyed by socio-political factors. Net-zero, renewable portfolio standards, and other clean energy emission goals and mandates, coupled with a new emphasis on environmental, social, and governance (ESG) initiatives, will accelerate the timing of coal plant retirements. ScottMadden projects the end of coal as an electric generation source in the United States sometime within this century.

Beginning in the early 2000s, one of the most significant trends in U.S. electric generation is the shift away from coal as a primary generation source. Previously, maxims such as “coal is king” were unquestioned in generation-related decision-making, but several factors disrupted the economics of coal generation, leading to the closure of coal plants. These included the rise of commercial-grade wind and solar renewables, the precipitous drop in natural gas prices driven by fracking, and the cost of retrofitting existing coal plants to meet more stringent environmental standards. While never an easy decision, closing a coal unit that was losing money, or projected to lose money, was a relatively straightforward strategy to articulate to boards, investors, customers, and other stakeholders.

While economics continue to play a role in today’s decisions to retire coal plants, the second wave of coal plant retirements is being ushered in by increasing societal pressure to reduce carbon emissions. This whitepaper explores ScottMadden’s view of the six primary drivers of the second wave. Our analysis is based on ScottMadden’s experience working with both large and small electric generation companies across North America, as they make strategic decisions about changes to their generation profiles.

Figure 1: U.S. Coal Plant Retirements, Actual and Projected 1970–2042[1]

CURRENT LANDSCAPE OF U.S. COAL GENERATION

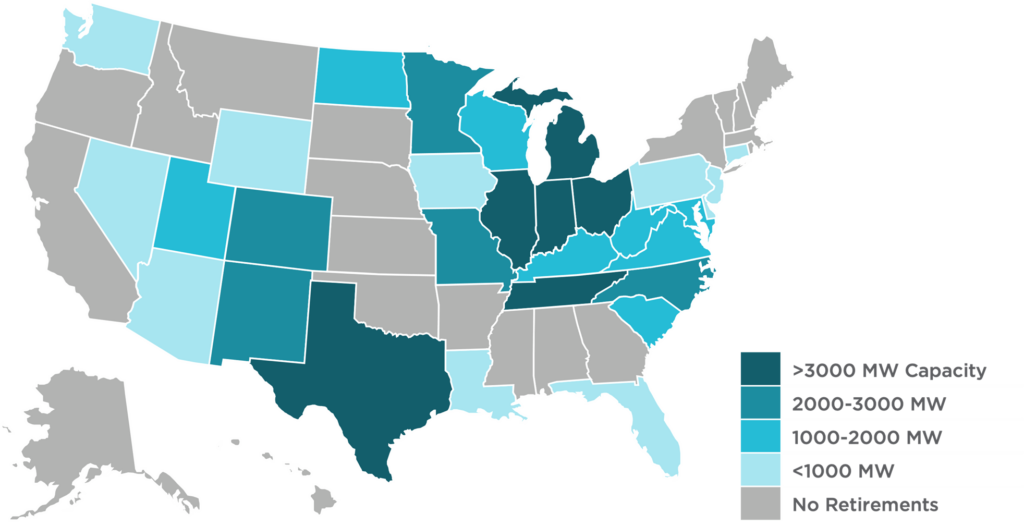

The United States has been home to nearly 500 grid-connected coal plants, representing more than 1,200 units. By 2020, however, fewer than 600 units continued to operate in the United States, representing an approximate capacity of 230 GW and an average age of 45 years. Today, roughly a third of that capacity (73 GWs) is set to retire by 2045.[2]

Figure 2: Planned Coal Generating Plant Retirements by State between 2022 and 2045[3]

While the United States saw a 17% increase in coal generation in 2021, the recent surge is attributable to high natural gas prices, as oil and natural gas producers curbed production amid the ongoing COVID-19 pandemic.[4] The surge in coal generation is no doubt temporary (see sidebar) as natural gas production returns to pre-pandemic levels, more U.S. coal plant closures are announced, and renewable generation continues to be built.

Historically, the age of a coal plant has been the best determinant of whether it will continue to operate. Since 2015, however, the emissions rate of a coal plant may have become a better indicator of that plant’s remaining life.[5] Figure 3 compares the average unit retired in 2015 with that in 2018.

…or is it?

Not everyone is abandoning coal quite yet, as natural gas prices have increased, motivating some recent gas-to-coal switching in some markets. While many mining companies were exiting the thermal coal market, some are responding to this recent uptick in demand by maintaining or growing investment in the sector. This is evidenced by Glencore Plc’s recent re-commitment to coal, at least through 2050. Glencore has promised to run down its coal assets by then, a plan approved by 94% of its shareholders, rather than divest the coal unit as urged by Bluebell Capital Partners.* This approach helped Glencore post record earnings in 2021, and coal is expected to be an even bigger contributor to Glencore’s profitability in 2022.**

This example may suggest that coal will be here longer than many think, driven by near-term investment opportunities and/or near-term energy security. This may be at odds with utilities and jurisdictions that have set net-zero targets.

*Financial Times: Glencore defends coal rundown strategy as right for the world, https://www.ft.com/content/81696e63-38c5-4454-8a03-8a92fdc4ca5a

**Miningmx: Nagle stands behind Glencore coal strategy with fuel set to drive EBITDA in 2022, https://www.miningmx.com/news/markets/48759-nagle-stands-behind-glencore-coal-strategy-as-fuel-set-to-drive-ebitda-in-2022/

Figure 3: Comparison of Average U.S. Units Retired in 2015 vs. 2018[6]

DRIVERS OF COAL PLANT CLOSURES

There are six primary drivers of this wave of U.S. coal plant closures. The first three relate to economics and financial decisions, while the last three are more socio-political in nature.

- Natural Gas Prices: The abundant supply of domestic natural gas reserves has reduced its cost, making it more attractive for electricity generation. By 2050, natural gas-fired generation is projected to remain in favor, comprising approximately 34% of the power generated in the United States, relatively flat from its 2021 share (37%).[7]

- Cost Competitiveness of Renewables: Renewable energy is rapidly becoming a more cost-competitive source of generation, benefiting from technological advances, state renewable portfolio standards and related policies, and (in the case of wind and solar) favorable tax treatment.

- Aging Units: The majority of U.S. coal capacity was built between 1970 and 1990. The average age of all operating coal units is currently 46 years, and 81% are more than 25 years old.[8] While they may still carry debt, these units are fully depreciated, which facilitates the decision to retire them.

- Public Perception of Coal: Public opinion of coal-fired generation has become increasingly negative over time. The process of burning coal to generate electricity is targeted by a wide range of groups that argue the practice is one of the primary causes of climate change and other public health problems, particularly respiratory ailments like asthma. The rise of ESG concerns has brought the energy industry into the spotlight, and utilities with coal-generating assets have increasingly been identified as targets of activism.

- Renewable Portfolio of Coal: The term RPS is often used interchangeably with renewable energy/electricity standards (RES). Both describe policies that require or encourage suppliers to provide customers with a minimum share of electricity from renewable resources. While there is no federal RPS policy, 31 states and DC have enacted their own policies with wide-ranging renewable energy targets and timelines, ranging from 8.5–100% and 2021–2050, respectively. No two states have the same requirements, and states frequently make significant revisions to RPS policies. In 2019 alone, eight states raised or set new RPS targets. As of early 2021, RPS policies covered 58% of total U.S. retail electricity sales, but this figure is higher today as states continue to update their standards. As more states adopt or raise RPS targets each year, that influence is expected to grow in the coming years.[9]

- Foreign and Domestic Focus on Climate Change: The recent release of the United Nations Intergovernmental Panel on Climate Change (IPCC) Report, which has been described as a “code red for humanity,” reinforces the international belief that a global shift away from fossil fuels is an urgent imperative.[10]

On day one of his presidency, Joe Biden rejoined the Paris Agreement, and made addressing climate change a central element of both foreign and domestic policy. Biden has created two new positions in the Office of the President: John Kerry as Special Presidential Envoy for Climate and Gina McCarthy as head of the White House Office of Domestic Climate Policy. Kerry is the first-ever principal to sit on the National Security Council entirely dedicated to climate change, and McCarthy, frequently described as the “Climate Czar,” coordinates domestic climate policy across agencies and departments.

IN CLOSING

The strategic process for building, operating, and retiring generation units is complex. These are big decisions that require input and analysis from many stakeholders. To date, the decision to close coal units in the near-term has been driven primarily by economics. While never easy, the process is straightforward for any executive when analyzing an asset that costs more to operate than it earns.

Going forward, ScottMadden predicts that while closures will continue to be driven by economic factors, public perception, RPS requirements, and an international focus on climate change will increasingly drive decision-making and trigger a second wave of coal plant closures, dramatically shifting generation away from coal to natural gas and renewables.

RELATED ARTICLES

This article is part of a series titled Coal’s Accelerated Burn covering coal unit closures.

- Drivers for Coal Unit Closures

- Management Guide to Coal Unit Closures

- Stakeholder Analysis: A Case Study

- After the Closure: What’s Next for a Decommissioned Coal Plant?

Additionally, we suggest the following article written by Dorsey & Whitney’s Development and Infrastructure Industry Group:

HOW SCOTTMADDEN CAN HELP

ScottMadden has assisted many generation companies to effectively analyze, plan, and execute coal plant decommissioning projects. We approach decommissioning work with a deep respect for the stakeholders and leverage our significant experience to support your initiatives. Our experience includes:

- Decommissioning analysis and strategy

- Decommissioning planning

- Stakeholder communications and employee notifications

- Project management

- Organizational redesign

- Reduction in force analysis and implementation

- Vendor selection for demolition/deconstruction

- Development of coal ash disposal strategy

- Decommissioned plant strategic repurposing analysis

For more information on how ScottMadden can assist you with coal plant decommissioning and other fossil generation initiatives, please contact us.

[1] S&P Global Market Intelligence, ScottMadden analysis

[2] EIA: Planned U.S. Electric Generating Unit Retirements, https://www.eia.gov/electricity/monthly/epm_table_grapher.php?t=epmt_6_06

[3] EIA: 2020 Form EIA-860 Data – Schedule 3, ‘Generator Data’ (Proposed Units Only) https://www.eia.gov/electricity/data/eia860/xls/eia8602020.zip

[4] Washington Post: U.S. emissions surged in 2021, putting the nation further off track from its climate targets, https://www.washingtonpost.com/climate-environment/2022/01/10/us-emissions-surged-2021-putting-nation-further-off-track-its-climate-targets/

[5] Scientific America: And Now the Really Big Coal Plants Begin to Close, https://www.scientificamerican.com/article/and-now-the-really-big-coal-plants-begin-to-close/

[6] EIA: More U.S. coal-fired power plants are decommissioning as retirements continue, https://www.eia.gov/todayinenergy/detail.php?id=40212

[7] EIA: Annual Energy Outlook 2022 with projections to 2050, http://www.eia.gov/forecasts/aeo/

[8] EIA: Detailed generator-specific information about existing and planned generators, https://www.eia.gov/electricity/data/eia860/

[9] Lawrence Berkeley National Laboratory: U.S. Renewables Portfolio Standards 2021 Status Update: Early Release, https://eta-publications.lbl.gov/sites/default/files/rps_status_update-2021_early_release.pdf

[10] Reuters: U.N. Climate Change Report Sounds ‘Code Red for Humanity,’ https://www.reuters.com/business/environment/un-sounds-clarion-call-over-irreversible-climate-impacts-by-humans-2021-08-09/